Tax Tips for Earning less than $21 per hour

The Florist - Ep 2. - $21/hr

Welcome back to the Florist. A fictional series of stories about a man who has found a secret tax AI engine that he has conversations with.

Our protagonist, Mr. Profitt the Florist flips open his laptop in the basement of his flower shop and powers on the program on the computer. He switches it and types in the following query. “Karen+Capone, pretend you are a tax professional in 2023 America and receive the following question: What is the best tax strategy for a single person earning $21 or less in W2 wage income”

The computer fans hummed, and the machine got hot before the following text began to print on the screen:

There are plenty of tax strategies out there on how to optimize your tax burden if you are an entrepreneur or multi state millionaire but what about ‘regular joe’ or ‘regular crypto joe’ just earning a living as a self employed entrepreneur or even more plainly a W2 wage earner.

Well, the reason you don’t see tax strategies for ‘regular joe’ is that ‘regular joe’ can’t afford to pay someone for awesome tax advice. So I’m going to give it away in an article. Why? Well, one of the greatest tax strategies for regular wage earners is also the foundation for a cohesive society and furtherance of God’s will for humanity. So here it goes.

Family Structure

The best tax advantage strategy for a person earning under $21, especially a single person, is to get married and have at least 2 children and have one spouse not work outside the home.

Did you just do an eyeroll to yourself? Did you just think “oh great, I bet he’s going to tell me to pull myself up by my bootstraps next”. Well you are wrong, this is not a boomer lecture. I’m going to show you real dollar examples of how much this tax strategy can save you.

For this example we’re going to use a single person earning $44,000 per year in a state with no income tax requirements as that just makes this harder. However, if you do live in a state with income taxes, it’s almost certain that you will do even better as those states also have generous tax benefits for moderate income families. Wisconsin and Minnesota come to mind without doing any research.

Joe

For our example we will call our model person Joe. Joe’s $44,000 in annual earnings results in $21.15 per hour. Federal income taxes are $3,524 along with about another $3,300 in self employment taxes. This results in a tax burden of $6824. Joe also pays $300/month for a silver tier health insurance plan from the marketplace, which puts him at $33,576 in income after that. Joe is also too busy to make lunch each day for work, which costs him $10/day or $2600/year. He also pays for a drop off laundry service because he is too busy which costs him $30/week or $1560. Joe also pays $516/month for his car payment, which is the average for used cars in 2023. He pays $100/month for insurance and $50/week for fuel. After his car expenses. Joe also rents a 1 bedroom apartment for $1753/month. All of this data is collected using average values for 2023.

Janet

We need a second person as well. Janet is also a single person, working as a Nanny. Janet earns $37,180 as a Nanny. She pays $2579 in income tax and $2844 in social security taxes. Janet also pays $300/month for silver tier health insurance from the health insurance marketplace for $3600/year. Janet is not a live in nanny and so has a car and commuting costs of $9992 like Joe. Janet has the same rental arrangement as Joe, renting a 1 bedroom apartment.

Not taxable Labor

Joe gets married to Janet and they have 2 children. Joe continues to work his same job and Janet gets a new job with incredible tax advantages. Janet becomes a stay at home mother. There is a secret in the tax code that all labor of a stay at home parent is NON TAXABLE. Lets not kid ourselves that Janet’s work isn’t valuable or quantifiable. We already quantified making lunch at $2600/year out of pocket for Joe and laundry at $1560. The cost of a nanny for 2 children is $715/week in 2021 or $37,180. So Janet is doing at least those 3 jobs combined for a value of $41,340 but she doesn’t have to pay income tax or social security tax on any of it. Joe and Janet are producing a combined $85340 of value but there is zero income tax or social security tax on Janet’s labor. That is $5,423 in tax savings for the couple. Janet is also no longer paying room and board costs, the couple is paying that to themselves for wherever they are renting or owning.

That isn’t even the good part. Lets move onto health insurance savings next.

Health Insurance

Remember, Janet and Joe were paying $300/month each for silver tier health insurance, so $600 total per month. Now that they are married and have 2 children and a taxable income of $44,000/year they qualify for health insurance subsidies. For an equivalent silver tier plan that covers Joe, Janet and their two children their cost is $25 per month to cover the entire family. Their insurance expenses have now gone from $7200 to $300 per YEAR. That is $6900 in savings, which is equivalent to Joe’s entire disposable income when he was single.

Income Taxes

Next up, lets do the taxes. Because they are married, they get an increased standard tax deduction and better tax bracket rates. Because all of Janet’s labor is now non taxable, those tax deductions all go to offset Joe’s wage income. Furthermore, because their taxable income is now $44,000 for the entire family and they have 2 children they also become eligible for Earned Income Tax Credits and the child tax credit. I am not going to detail the entire return but the outcome is that not only do they owe zero income tax on Joes’ wages but they get a refund of $4610. There is still $3300 in social security taxes due on Joe’s income though. When they were single, Joe and Janet paid $9,688 in combined taxes. They are now getting a refund of $1310. That is a change of $10,998 in tax expenditures. That was almost their entire amount of disposable income previously.

Living Costs

Lets tackle living space next. Prior to being married Joe and Janet spent $21,036 each for one bedroom apartments. Their total outlay was $42,072/year. Now that they are married with children they rent a 2 bedroom apartment at a cost of $25,440/year. The children share a bedroom. That is a savings of $16,632 but is also not some kind of eye popping revelation.

Last, lets do vehicles. Joe and Janet are going to really buckle down and go down to one vehicle. Being at home most of the time Janet either does not need the vehicle, or drops Joe off at work on the days she does. Going down to one vehicle saves them $9792.

Summary

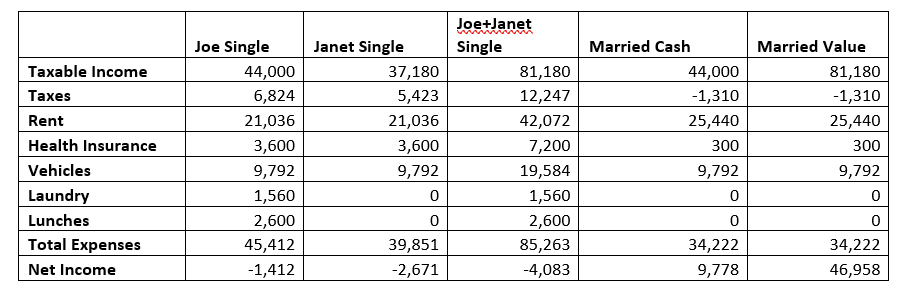

I’ve summarized the outcomes in the following table. The columns are each individuals’ expenses and income while single and then summed together. There is a column representing their cash taxable income while married and then a final one representing their income value while married.

The first obvious comment is that Joe and Janet have a negative income while single. While this seems impossible, this is also realistic given the inflation of goods that are present in 2023 leading to skyrocketing consumer debt. Joe and Janet could cut costs by getting roommates or cheaper cars or places to live but that is true across all scenarios. The fact that neither person can pay ‘average’ costs while making $21 per hour is a large societal issue.

Invest in yourselves

The second commentary is to the married cash value. Despite living only on Joe’s wage income this married family of 4 can have a surplus income of $9778. That surplus will likely get spent on food and utilities but is still almost $15,000 greater than when Joe and Janet were trying to make it on their own. Last, the “Married Value” is astounding. When putting a dollar value on Janet’s in home labor the married family has a net surplus of $46,958. This is not realized in dollars as the value of Janet’s labor is reinvested in caring for their children and household but it is still value. What used to be paid as wages for her to nanny other children is now realized as raising her own children with a surplus cash result. In the other scenarios denominated in dollars only, Janet and Joe’s labor is still worth the same but it is being distributed to others instead of their own family. That is to say landlords, tax collectors and auto loans are realizing the value of their labor instead of their family. Would you rather have the fruits of your labor going to someone else, or to your own family primarily?

I did run two other scenarios which I did not publish here. That is Joe and Janet being married with no children and just Joe working. That created a cash surplus of $976, which is grossly worse than $9778 with children but still much better than -$4083 and that savings is primarily by just sharing a 1 bedroom apartment. I also ran a scenario where Joe and Janet both work while married with no children. This resulted in a net cash position of $12,888 versus $9,778 with 2 children but again in this situation all of the value of Joe and Janet’s labor is being extracted by others and fully taxed by the government.

…end of output.

Mr. Profitt read through the scenario output by the computer AI and sighed to himself “wow, things in 2023 sure were tough. Well they didn’t have to deal with thought crimes and terminator drones like we do now, but harder to pay the bills back then.”

End of Episode.